Low cost medical insurance for couples helps you and your partner protect your health without breaking the bank. With rising healthcare expenses, finding a plan that offers comprehensive coverage at an affordable price is essential. From shared deductibles to family-friendly benefits, these plans are designed to give you peace of mind while keeping your budget in check.

Key Takeaways

- Affordable Coverage: Low cost medical insurance for couples allows you to share premiums, making healthcare more budget-friendly than individual plans.

- Shared Benefits: Many plans offer combined deductibles and out-of-pocket maximums, reducing overall expenses when both partners use care.

- Family-Friendly Options: Most couple-focused plans include coverage for children, offering extended protection without extra costs.

- Flexible Plan Types: From HMOs to PPOs, you can choose a plan that fits your lifestyle and preferred healthcare providers.

- Tax Advantages: Premiums paid through employer-sponsored plans may be tax-deductible, lowering your overall financial burden.

- Preventive Care Included: Many low cost medical insurance plans cover routine check-ups, vaccinations, and screenings at no extra charge.

- Online Enrollment: Most providers offer easy digital sign-ups, comparison tools, and customer support to simplify the process.

📑 Table of Contents

- Low Cost Medical Insurance for Couples: A Smart, Affordable Way to Stay Healthy Together

- Why Choose Low Cost Medical Insurance for Couples?

- Types of Low Cost Medical Insurance Plans for Couples

- What’s Covered Under Low Cost Medical Insurance for Couples?

- How to Choose the Right Low Cost Medical Insurance Plan

- Tips for Saving Even More on Low Cost Medical Insurance for Couples

- Real-Life Example: How Sarah and Mike Saved $2,400 a Year

- Common Myths About Low Cost Medical Insurance for Couples

- Final Thoughts: Protecting Your Future Together

Low Cost Medical Insurance for Couples: A Smart, Affordable Way to Stay Healthy Together

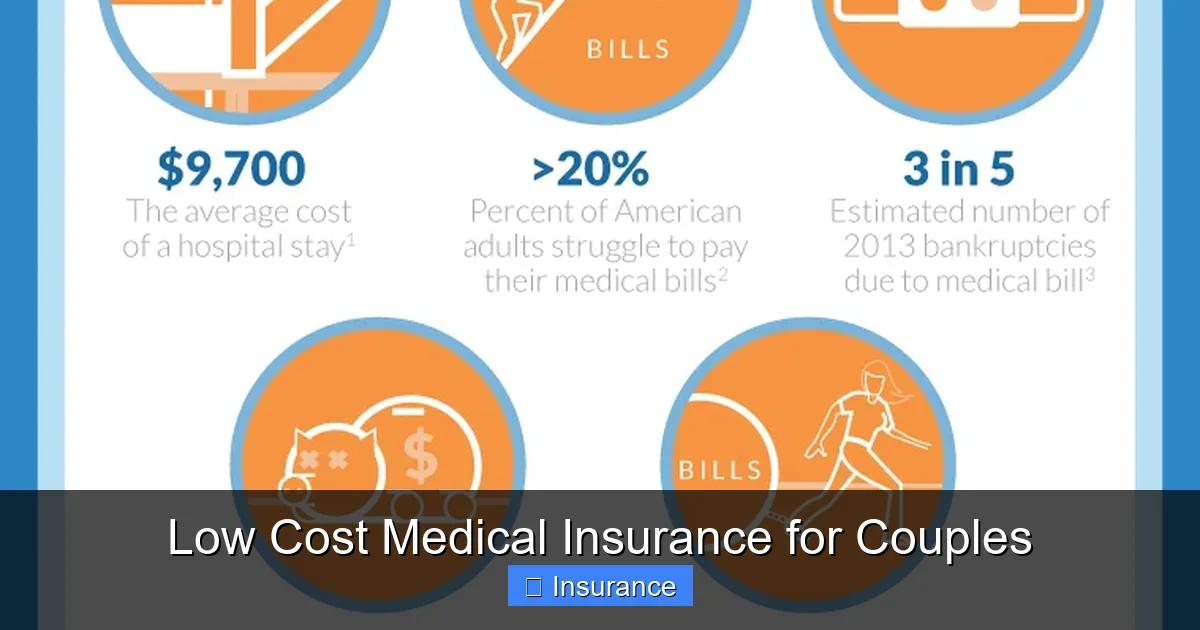

Raising a family or building a life with your partner means more than just shared dreams—it means shared responsibilities. One of the most important responsibilities is protecting your health and financial future. With healthcare costs rising faster than inflation, finding a medical insurance plan that works for both of you can feel overwhelming. But what if you could get comprehensive coverage without the hefty price tag?

That’s where low cost medical insurance for couples comes in. These plans are specifically designed for partners who want to combine coverage, reduce premiums, and still access quality care. Whether you’re newly engaged, married, or simply living together, a joint plan can offer peace of mind, financial savings, and streamlined benefits. In this guide, we’ll walk you through everything you need to know—from understanding how these plans work to choosing the best one for your needs.

Why Choose Low Cost Medical Insurance for Couples?

When two people are covered under one medical insurance plan, the cost savings can be significant. Instead of paying separate premiums, you split the cost, often resulting in lower monthly bills. But it’s not just about saving money—it’s about smart planning. Let’s break down the key reasons why couples should consider this option.

Visual guide about Low Cost Medical Insurance for Couples

Image source: lowcost.health

1. Lower Premiums Through Shared Coverage

One of the biggest advantages of low cost medical insurance for couples is the ability to share premium payments. Most insurance providers offer discounted rates when both partners are on the same plan. For example, if a plan costs $600 per month for an individual, a couple plan might cost only $800–$900 total. That’s a savings of hundreds of dollars each month.

Imagine saving over $1,000 annually just by combining your plans. Over time, those savings can go toward building an emergency fund, paying off debt, or even covering out-of-pocket medical expenses.

2. Simplified Billing and Claims

Having one policy means one bill, one ID card, and one point of contact for customer service. This simplifies the entire process—especially when you’re juggling work, family, and healthcare needs. Instead of tracking two separate insurance cards and two sets of paperwork, everything is centralized.

Additionally, many providers offer digital tools that let you manage your coverage, view claims, and access your member portal from your phone. This modern approach saves time and reduces stress.

3. Comprehensive Coverage for Both Partners

Low cost medical insurance for couples doesn’t mean cutting corners on benefits. In fact, most plans offer full coverage for both individuals, including doctor visits, hospital stays, emergency care, prescription drugs, and preventive services.

For example, if one partner needs surgery and the other needs a routine check-up, the plan covers both without requiring separate deductibles. This flexibility ensures that both of you get the care you need, when you need it.

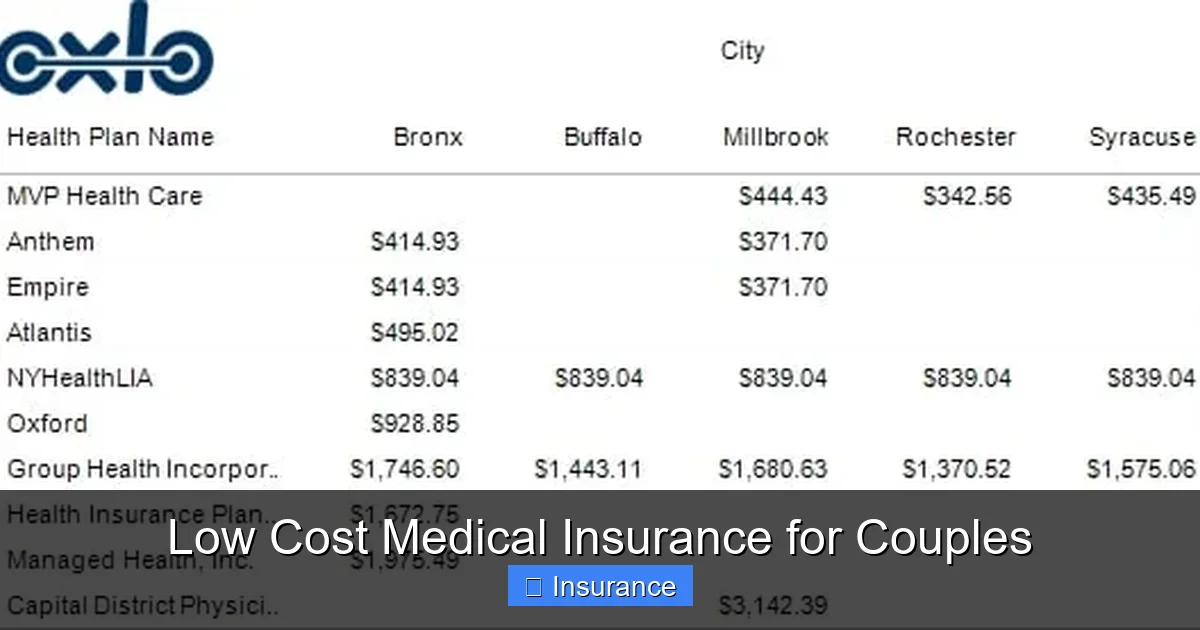

Types of Low Cost Medical Insurance Plans for Couples

Not all insurance plans are created equal. When choosing a plan, it’s important to understand the different types available. Each has its own strengths and limitations. Here’s a breakdown of the most common options.

Visual guide about Low Cost Medical Insurance for Couples

Image source: blog.oxlo.com

1. Health Maintenance Organization (HMO)

HMO plans are popular for their low premiums and comprehensive coverage. The key feature? You must choose a primary care physician (PCP) and get referrals to see specialists. While this can limit flexibility, it often results in lower out-of-pocket costs.

Best for: Couples who prefer a structured healthcare system and don’t mind seeing doctors within a network.

2. Preferred Provider Organization (PPO)

PPO plans offer more freedom. You can see any doctor or specialist without a referral, even outside the network. However, going outside the network will cost more. This makes PPOs ideal for couples who want flexibility but still want to save on costs.

Best for: Couples who value choice and want to visit specialists or out-of-network providers without jumping through hoops.

3. High-Deductible Health Plans (HDHP)

HDHPs have lower monthly premiums but higher deductibles. These plans are often paired with Health Savings Accounts (HSAs), which allow you to save pre-tax dollars for medical expenses. If you’re generally healthy and don’t expect major medical bills, this can be a smart financial move.

Best for: Young, healthy couples who want to minimize monthly payments and take advantage of tax-free savings.

4. Catastrophic Plans

Available to people under 30 or those with hardship exemptions, catastrophic plans have very low premiums and high deductibles. They cover essential health benefits after the deductible is met and are designed to protect against worst-case scenarios—like a serious illness or injury.

Best for: Young couples in good health who want emergency protection without long-term commitments.

What’s Covered Under Low Cost Medical Insurance for Couples?

Understanding what your plan covers is just as important as understanding the cost. Let’s look at the standard benefits included in most low cost medical insurance plans.

Visual guide about Low Cost Medical Insurance for Couples

Image source: miro.medium.com

1. Preventive Care

Most plans cover preventive services at no extra cost. This includes annual physicals, vaccinations, cancer screenings, and wellness visits. Early detection saves money and lives, so this is a huge benefit.

Example: If you and your partner both need a mammogram or colonoscopy, the plan covers it—no co-pay, no waiting.

2. Emergency Services

Accidents happen. Whether it’s a broken bone from a fall or a sudden illness, emergency room visits are typically covered. Some plans may have a co-pay or coinsurance, but they won’t leave you with a surprise bill.

3. Hospitalization and Surgery

Overnight hospital stays, surgeries, and related services are covered under most plans. This includes pre- and post-operative care, anesthesia, and recovery services.

4. Prescription Drugs

Many plans include a formulary—a list of approved medications—with tiered pricing. Generic drugs are usually the most affordable, while brand-name drugs may require a higher co-pay.

5. Mental Health and Substance Abuse Services

Modern plans recognize the importance of mental health. Counseling, therapy, and substance abuse treatment are often covered, sometimes with no deductible.

6. Maternity and Family Planning

If you’re planning to start a family, look for plans that cover maternity care, fertility treatments, and family planning services. Some even offer prenatal and postnatal care at no extra cost.

How to Choose the Right Low Cost Medical Insurance Plan

With so many options, picking the right plan can feel like navigating a maze. But don’t worry—we’ve got you covered. Here’s a step-by-step guide to help you make the best decision.

1. Assess Your Health Needs

Start by evaluating your health history and current needs. Do you or your partner have chronic conditions? Do you take regular medications? Are you planning to start a family?

If you’re both healthy and don’t expect major medical issues, a high-deductible plan with an HSA might be ideal. If one of you has ongoing health concerns, a plan with lower out-of-pocket costs could be better.

2. Compare Premiums, Deductibles, and Out-of-Pocket Maximums

Look beyond the monthly premium. A plan with a low premium might have a high deductible, meaning you’ll pay more out of pocket before coverage kicks in. Use a comparison tool to see the total estimated cost for the year.

Tip: Aim for a balance. A plan that’s slightly more expensive but covers most of your expected expenses can save you money in the long run.

3. Check the Provider Network

Make sure your preferred doctors, hospitals, and specialists are in-network. If you have a trusted primary care physician, confirm they accept your insurance before signing up.

4. Review Customer Service and Support

Choose a provider with good customer service. Look for companies with 24/7 support, online chat, and user-friendly apps. A responsive insurer can make a big difference when you need help.

5. Consider Add-Ons and Riders

Some plans offer optional add-ons like dental, vision, or mental health coverage. If you need these, factor them into your decision. Others, like critical illness riders, can provide extra financial protection.

Tips for Saving Even More on Low Cost Medical Insurance for Couples

You’ve found a great plan—now how can you save even more? Here are some practical tips to stretch your budget further.

1. Use In-Network Providers

Sticking to in-network doctors and hospitals can save you hundreds or even thousands of dollars. Always confirm before scheduling an appointment.

2. Take Advantage of Preventive Care

Since preventive services are usually covered at 100%, make sure you and your partner use them regularly. This helps catch problems early and avoids costly treatments later.

3. Use a Health Savings Account (HSA)

If you have a high-deductible plan, open an HSA. You can contribute pre-tax dollars, and the money grows tax-free. Use it to pay for qualified medical expenses—no strings attached.

4. Shop Around During Open Enrollment

Most people shop for insurance only once a year. But during open enrollment, you can compare new plans and switch if something better comes along. Don’t miss this window!

5. Bundle with Other Insurance

Some insurers offer discounts if you bundle your medical plan with auto, home, or life insurance. Ask your provider if bundling is an option.

6. Negotiate Medical Bills

If you receive a large bill, don’t pay it immediately. Call the provider and ask if they offer a discount for prompt payment or financial hardship. Many hospitals are willing to work with you.

Real-Life Example: How Sarah and Mike Saved $2,400 a Year

Sarah and Mike, a couple in their early 30s, both worked part-time jobs with limited benefits. They were paying $500 each per month for separate individual plans—totaling $12,000 a year. After doing some research, they switched to a shared low cost medical insurance plan that cost only $750 per month for both of them.

Not only did they save $5,400 annually on premiums, but the new plan also covered their two young children at no extra cost. They used the savings to build an emergency fund and even took a vacation. “We felt like we were getting ripped off before,” Mike said. “Now we have real peace of mind.”

This is just one example—but it shows how powerful smart insurance choices can be.

Common Myths About Low Cost Medical Insurance for Couples

There are a lot of misconceptions about affordable health insurance. Let’s clear up some of the most common myths.

Myth 1: “Cheap Insurance Means Poor Coverage”

False. Many low cost medical insurance plans offer comprehensive benefits. The key is choosing the right plan for your needs and understanding the trade-offs.

Myth 2: “You Can’t Get Good Care with a Couple Plan”

False. As long as your doctors are in-network, you’ll receive the same quality care as with any other plan. In fact, some plans offer better coordination between partners’ care.

Myth 3: “Only Married Couples Can Use These Plans”

False. Most providers allow unmarried couples to enroll, especially if they live together and share financial responsibilities. Check the specific rules with your insurer.

Myth 4: “You Have to Wait to Enroll”

False. While open enrollment is the best time to sign up, many plans allow new enrollments during special circumstances like marriage, birth, or loss of other coverage.

Final Thoughts: Protecting Your Future Together

Choosing low cost medical insurance for couples isn’t just about saving money—it’s about investing in your shared future. Health is wealth, and having reliable coverage means you’re both protected, no matter what life throws your way.

Whether you’re starting a family, managing chronic conditions, or just want to be prepared, a well-chosen plan can make all the difference. Take the time to compare options, ask questions, and choose a plan that fits your lifestyle and budget.

Remember, the best insurance isn’t the cheapest—it’s the one that gives you confidence, security, and peace of mind. And when you and your partner are covered together, you’re not just saving money. You’re building a stronger, healthier life—side by side.

Frequently Asked Questions

Can unmarried couples get low cost medical insurance?

Yes, many insurers allow unmarried couples to enroll in shared plans, especially if they live together and share financial responsibilities. Policies may vary by provider, so it’s best to check eligibility requirements.

Are low cost medical insurance plans worth it?

Absolutely. These plans offer comprehensive coverage at a fraction of the cost of individual policies. With shared premiums, preventive care, and family benefits, they’re a smart choice for couples.

What’s the difference between an HMO and a PPO?

HMO plans require a primary care physician and referrals for specialists but offer lower costs. PPO plans allow more flexibility to see any doctor without referrals, though out-of-network care costs more.

Can I add children to a couple’s insurance plan?

Yes, most low cost medical insurance plans for couples include coverage for dependent children. This often comes at no extra premium, making it a great value for families.

How do I know if a plan is right for me?

Consider your health needs, budget, and preferred providers. Compare premiums, deductibles, and network options. Using a comparison tool or consulting a licensed agent can help you make the best choice.

When is the best time to enroll in a couple’s insurance plan?

Open enrollment (usually fall) is the ideal time, but you can also enroll during special life events like marriage, birth, or job loss. Missing open enrollment doesn’t mean you can never sign up again.