Medical insurance claim rejections can be frustrating and costly. Understanding why claims get denied helps you avoid common pitfalls. By knowing the top reasons for rejection, you can take action to fix errors and resubmit successfully.

Medical insurance claim rejection reasons can leave patients confused, frustrated, and facing unexpected bills. When your health is on the line, getting reimbursed for medical expenses should be straightforward—but it’s not always. Insurance companies process thousands of claims daily, and even small mistakes can lead to denial.

Understanding why medical insurance claims get rejected is the first step toward avoiding these issues. This guide walks you through the most common medical insurance claim rejection reasons, explains how to spot them, and offers practical tips to prevent future denials. Whether you’re filing a claim for yourself or helping a family member, this knowledge will help you navigate the system more effectively.

Key Takeaways

- Incorrect or missing information: Simple errors like typos or incomplete forms are common causes of claim denial.

- Out-of-network services: Using providers not in your insurance network often leads to claim rejection.

- Non-covered services: Cosmetic procedures or experimental treatments are frequently denied by insurers.

- Timely filing issues: Missing deadlines for claim submission is a frequent reason for rejection.

- Duplicate claims: Submitting the same claim multiple times can trigger automatic denial.

- Lack of medical necessity: Insurers often deny claims if they don’t believe treatment was essential.

- Coordination of benefits errors: Failing to report secondary insurance leads to processing delays.

📑 Table of Contents

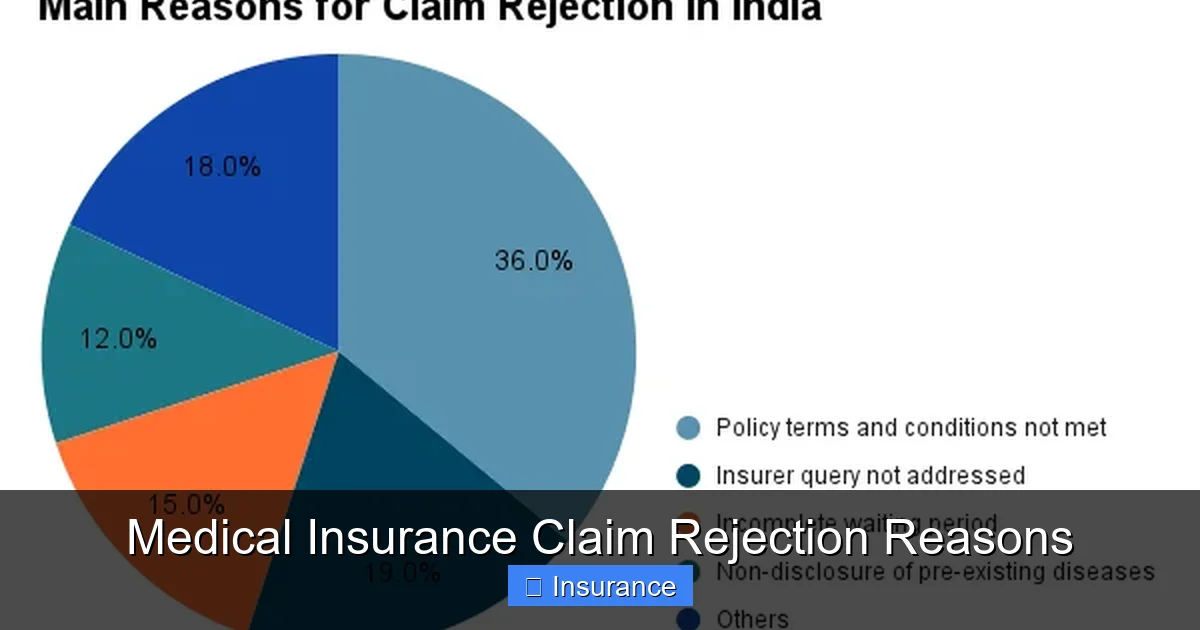

Common Medical Insurance Claim Rejection Reasons

1. Incorrect or Missing Information

One of the most frequent medical insurance claim rejection reasons is simply not providing the right information. Insurance forms require precise details, and even minor errors can trigger denial. This includes incorrect patient IDs, misspelled names, or missing diagnosis codes.

For example, if your policy number has a typo or your date of birth is entered incorrectly, the insurer may reject the claim outright. Similarly, if the provider forgets to include the correct CPT (Current Procedural Terminology) or ICD-10 (International Classification of Diseases) codes, the claim won’t process.

Pro tip: Always double-check all fields before submitting. Ask your healthcare provider to verify codes and patient details. Many rejections can be avoided with a quick review.

2. Out-of-Network Providers

Using healthcare providers outside your insurance network is a major reason for medical insurance claim rejection. Insurance plans typically cover a higher percentage of costs when you use in-network doctors, hospitals, and clinics.

If you visit an out-of-network provider without prior authorization, your claim may be denied. Even if the service was necessary, the insurer may refuse to pay unless you had approval in advance. This is especially common with specialists, urgent care centers, or emergency rooms in unfamiliar cities.

Tip: Always confirm whether a provider is in-network before receiving care. Use your insurer’s online directory or call customer service to verify.

3. Non-Covered Services

Not all medical services are covered by insurance. Cosmetic procedures, experimental treatments, and certain preventive care options may be excluded from your plan. When you submit a claim for a non-covered service, it will likely be rejected.

Examples include:

- Laser eye surgery (unless medically necessary)

- Weight loss programs not related to obesity

- Alternative therapies like acupuncture or herbal supplements

- Elective cosmetic procedures

Even if the service was performed correctly, it won’t be reimbursed if it’s not part of your policy. Always review your Summary of Benefits and Coverage (SBC) to understand what’s included.

4. Timely Filing Issues

Insurance companies have strict deadlines for submitting claims—known as timely filing limits. These vary by plan but typically range from 90 to 365 days from the date of service.

If you submit a claim after this window, it will be rejected. This is one of the most preventable medical insurance claim rejection reasons. Many patients assume they have more time, especially if they’re dealing with complex treatments or multiple providers.

Example: A patient receives physical therapy on January 10th but doesn’t request reimbursement until March 1st. If the plan has a 60-day filing limit, the claim is denied.

Solution: Keep track of service dates and set reminders. Ask your provider to help you file promptly.

5. Duplicate Claims

Submitting the same claim more than once is a common cause of denial. This can happen accidentally when multiple staff members process the same invoice or when you file a claim after already receiving payment.

Insurance systems automatically flag duplicates. Even if the second claim is for a different patient, the system may reject it due to matching billing codes or provider information.

Tip: Keep a record of all submitted claims. If you’re unsure whether a claim was processed, contact your insurer before resubmitting.

6. Lack of Medical Necessity

Insurers assess whether a medical service was truly necessary for your health. If they determine the treatment wasn’t essential, they may deny the claim. This often happens with diagnostic tests, surgeries, or medications.

For instance, an MRI might be denied if the insurer believes it wasn’t needed based on your symptoms or prior records. Similarly, a specialist referral may be rejected if it wasn’t pre-authorized.

Prevention: Always get pre-authorization for major procedures. Ask your doctor to explain why a test or treatment is medically necessary before scheduling it.

How to Avoid Medical Insurance Claim Rejections

1. Review Your Policy Thoroughly

Understanding your insurance plan is your best defense against denial. Read your policy documents carefully, including the Summary of Benefits and Coverage. Pay attention to:

- What services are covered

- What requires pre-authorization

- Network provider requirements

- Filing deadlines

- Out-of-pocket maximums and deductibles

Visual guide about Medical Insurance Claim Rejection Reasons

Image source: blog.shoonya.com

When you know your coverage, you can make informed decisions about your healthcare and avoid surprises later.

2. Verify Provider Network Status

Before scheduling an appointment, confirm that your doctor or hospital is in-network. You can usually find this information on your insurer’s website or by calling customer service. Even if a provider seems reputable, they may have recently changed networks.

For urgent care or emergencies, note that some plans cover out-of-network services at a lower rate. But for routine care, staying in-network saves money and reduces denial risk.

3. Use Correct Billing Codes

Accurate coding is critical. Incorrect or outdated codes can lead to claim rejection. Make sure your healthcare provider uses the right:

- CPT codes (for procedures)

- ICD-10 codes (for diagnoses)

- Modifiers (to explain special circumstances)

If you’re unsure, ask your provider for a copy of the explanation of benefits (EOB) or itemized bill. This shows exactly what was billed and why.

4. File Claims Promptly

Set reminders to file claims within the timely filing window. Many patients delay filing because they’re waiting for final bills or dealing with co-pays. But waiting too long can result in denial.

Tip: Use a calendar or app to track service dates and deadlines. Some providers offer online portals where you can submit claims directly.

5. Communicate with Your Healthcare Provider

Your provider’s office plays a key role in claim processing. Ask them to:

- Confirm all patient information is correct

- Include necessary pre-authorization numbers

- Explain why a service was medically necessary

- Submit claims on time

Many rejections happen because of provider errors, not patient mistakes. A quick call can prevent a denial.

What to Do When Your Claim Is Denied

1. Review the Explanation of Benefits (EOB)

When a claim is denied, your insurer sends an Explanation of Benefits (EOB). This document explains why the claim was rejected and what you can do next. Read it carefully—it’s your roadmap to appealing the decision.

Visual guide about Medical Insurance Claim Rejection Reasons

Image source: even.in

Look for:

- The specific denial reason

- The claim reference number

- Instructions for appeal

- Deadlines for resubmission

Don’t ignore the EOB. It contains vital information that can help you correct the issue.

2. Gather Supporting Documentation

If you plan to appeal, collect all relevant documents:

- Medical records

- Doctor’s notes explaining medical necessity

- Pre-authorization letters

- Receipts and bills

Having strong evidence increases your chances of a successful appeal. Be thorough and organized.

3. Submit an Appeal

Most insurers allow you to appeal a denial within 60–180 days. Follow their appeal process exactly. Include a clear letter explaining why you believe the claim should be paid.

Example: “My claim for physical therapy on March 15, 2024, was denied due to lack of medical necessity. However, my doctor provided documentation showing the therapy was essential for my recovery from a work injury. Please reconsider.”

Keep copies of everything you send.

4. Contact Your Insurer

If you’re unsure why your claim was denied, call your insurance company. Ask for a detailed explanation. Sometimes, the reason isn’t clear from the EOB, and a conversation can clarify the issue.

Ask to speak with a claims specialist. They can guide you on next steps and help resolve the problem faster.

Preventing Future Claim Denials

1. Keep Accurate Records

Maintain a file of all medical visits, bills, and correspondence with your insurer. Include:

- Appointment dates

- Billing statements

- EOBs

- Appeal letters

Visual guide about Medical Insurance Claim Rejection Reasons

Image source: insurancesamadhan.com

This helps you track what’s been submitted and when. It also makes it easier to dispute errors.

2. Use Online Portals

Many insurers offer online portals where you can:

- View claims status

- Download EOBs

- Submit appeals

- Contact customer service

These tools save time and reduce paperwork. Make it a habit to check your portal regularly.

3. Ask Questions

Don’t assume you understand your insurance. Ask questions like:

- “Is this provider in-network?”

- “Do I need pre-authorization for this test?”

- “What’s the timely filing deadline?”

Your insurer wants to help—but only if you ask.

4. Consider a Medical Advocate

If you frequently face claim denials, a medical advocate or billing specialist can help. They review bills, negotiate with insurers, and assist with appeals. This service is especially useful for people with chronic conditions or complex medical histories.

Conclusion

Medical insurance claim rejection reasons are often preventable. By understanding the common causes—like incorrect information, out-of-network care, or untimely filing—you can take steps to avoid denials. The key is to be proactive: review your policy, verify providers, file claims on time, and keep accurate records.

When a claim is denied, don’t give up. Review the EOB, gather evidence, and submit a well-documented appeal. With persistence and attention to detail, most denials can be resolved.

Remember, your health is worth fighting for. By staying informed and organized, you can reduce stress and ensure you get the coverage you deserve.

Frequently Asked Questions

Why was my medical insurance claim denied?

Common reasons include incorrect patient information, out-of-network providers, non-covered services, or untimely filing. Review your Explanation of Benefits (EOB) to identify the specific denial reason and take corrective action.

Can I appeal a denied insurance claim?

Yes, most insurers allow appeals within 60–180 days of denial. Gather medical records and a clear explanation from your doctor, then submit a formal appeal following your insurer’s process.

How long do I have to file a medical insurance claim?

Timely filing deadlines vary by plan but are typically 90 to 365 days from the date of service. Check your policy or contact your insurer to confirm your deadline.

What happens if I use an out-of-network provider?

Your claim may be denied or reimbursed at a lower rate. To avoid this, confirm your provider is in-network before receiving care and get pre-authorization when required.

Can duplicate claims cause denial?

Yes, submitting the same claim more than once will result in automatic denial. Keep records of all submitted claims and avoid resubmitting without confirmation.

How can I prevent claim denials in the future?

Review your policy, verify provider network status, use correct billing codes, file claims promptly, and maintain accurate records. Communicate with your healthcare provider to ensure all documentation is complete.