Medical insurance deductible vs copay are two key cost-sharing methods that affect how much you pay for healthcare. A deductible is what you pay out-of-pocket before insurance starts covering most services, while a copay is a fixed amount you pay for each visit or service. Understanding both helps you budget for medical expenses and avoid surprise bills.

Key Takeaways

- Deductible: The amount you pay before insurance covers most costs. High deductible plans often have lower premiums but higher out-of-pocket expenses initially.

- Copay: A fixed fee you pay for specific services like doctor visits or prescriptions, usually after meeting your deductible.

- Out-of-Pocket Maximum: The most you’ll pay in a year, including deductible, copays, and coinsurance. After this, insurance covers 100%.

- Plan Type Matters: HMOs, PPOs, and HDHPs each handle deductibles and copays differently—understand your network and coverage rules.

- Cost vs. Convenience: Low deductible plans mean more predictable costs but higher monthly premiums; high deductible plans save on premiums but require more upfront spending.

- Prescription Coverage: Copays apply to medications, but deductibles may delay coverage until you meet the threshold.

- Tax Advantages: HSAs and FSAs allow you to save pre-tax money for deductibles and copays, reducing your overall healthcare costs.

📑 Table of Contents

- Medical Insurance Deductible vs Copay Explained: What’s the Difference?

- What Is a Medical Insurance Deductible?

- What Is a Copay?

- Deductible vs Copay: Key Differences

- How Deductibles and Copays Affect Your Wallet

- How to Choose Between High and Low Deductible Plans

- Tips for Managing Deductibles and Copays

- Common Misconceptions About Deductibles and Copays

- Conclusion: Make Informed Choices About Your Health Plan

Medical Insurance Deductible vs Copay Explained: What’s the Difference?

Let’s face it—health insurance can feel like learning a new language. Between terms like “premium,” “coinsurance,” and “out-of-pocket maximum,” it’s easy to get lost. But two terms you’ll hear over and over are deductible and copay. These are the building blocks of how your health plan shares costs with you.

Think of your health insurance like a car insurance policy. Your premium is what you pay monthly. When you file a claim, your insurance kicks in—but how much you actually pay depends on the terms of your plan. In health insurance, the deductible and copay are those key terms. Understanding them helps you avoid sticker shock at the doctor’s office or pharmacy.

In this article, we’ll break down exactly what deductibles and copays are, how they differ, and how they affect your wallet. Whether you’re shopping for a new plan or trying to understand your current one, this guide will give you the clarity you need. Let’s dive in.

What Is a Medical Insurance Deductible?

A deductible is the amount you must pay out of pocket for covered healthcare services before your insurance plan starts to pay. It’s like a waiting period for your insurance coverage. Once you’ve met your deductible, your plan begins covering a larger share of your medical expenses.

Visual guide about Medical Insurance Deductible Vs Copay Explained

Image source: sommedicalpractice.com

How Deductibles Work in Practice

Imagine you have a plan with a $1,500 deductible. That means you’ll pay the first $1,500 of covered services yourself. After that, your insurance may cover 80% of the remaining costs, depending on your plan’s coinsurance terms.

For example, let’s say you go to the doctor and the visit costs $300. Since you haven’t met your $1,500 deductible yet, you pay the full $300. Later, you have surgery costing $10,000. You’d pay the remaining $13,500 after meeting your deductible—until you hit your out-of-pocket maximum.

Types of Deductibles

Not all deductibles are the same. Here are the main types:

- Individual Deductible: The amount you must pay if you’re the only person on the plan.

- Family Deductible: The total amount your family must pay collectively before coverage kicks in. Some plans require each family member to meet the deductible, while others have a combined limit.

For instance, a family plan might have a $3,000 individual deductible and a $6,000 family deductible. If your spouse has a $2,000 procedure and you have a $1,500 procedure, your family has now met $3,500—still short of the $6,000 family deductible.

Deductibles and Preventive Care

Good news: preventive services like annual checkups, vaccinations, and mammograms are often covered at 100% even before you meet your deductible. This means you can get these services without paying anything out of pocket.

So if your doctor recommends a flu shot or a wellness visit, you won’t touch your deductible. That’s one way insurance encourages healthy habits.

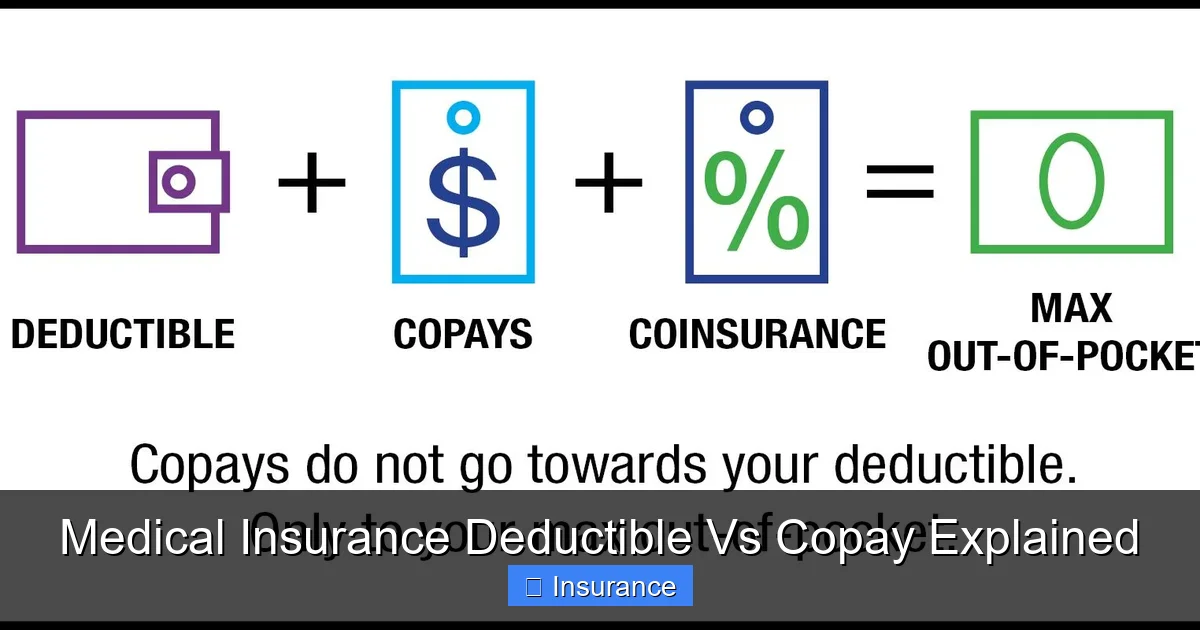

What Is a Copay?

A copay (short for “copayment”) is a fixed amount you pay for a covered healthcare service, usually at the time of service. Unlike a deductible, which you pay toward a cumulative total, copays are per-service fees.

Visual guide about Medical Insurance Deductible Vs Copay Explained

Image source: comproins.com

Common Copay Examples

Copays are typically used for routine or predictable services. Here’s a look at common copay amounts:

- Primary Care Visit: $20–$40

- Specialist Visit: $30–$60

- Urgent Care: $30–$50

- Emergency Room: $100–$300 (and sometimes more)

- Prescription (Generic): $10–$20

- Prescription (Brand Name): $30–$50

These copays are usually due when you receive the service. You might pay $25 at the doctor’s office, and the rest is billed to your insurance.

When Copays Apply

Copays generally apply after you’ve met your deductible. So if your plan has a $1,000 deductible and a $25 primary care copay, you’ll pay the full cost of your visit until you’ve paid $1,000 in total expenses. After that, you’ll pay the $25 copay for future primary care visits.

However, some plans allow copays to count toward your deductible. That means your $25 copay might count as part of the $1,000 you need to meet. Always check your plan details—this can save you money.

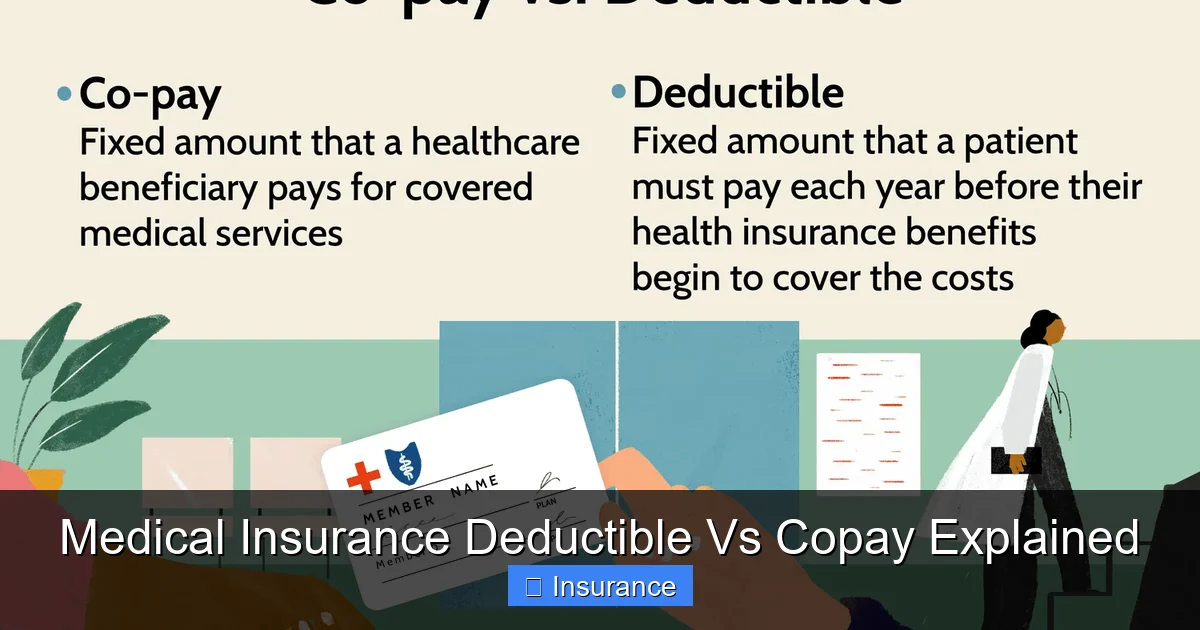

Deductible vs Copay: Key Differences

While both deductibles and copays are ways you share costs with your insurance, they work in very different ways. Let’s compare them side by side.

Visual guide about Medical Insurance Deductible Vs Copay Explained

Image source: investopedia.com

Timing and Frequency

- Deductible: You pay this toward a cumulative total. It’s not a per-service fee.

- Copay: You pay this each time you receive a service.

For example, if you have a $2,000 deductible and visit the doctor four times at $100 each, you’ll pay $400 toward your deductible. Your insurance won’t pay anything until you hit $2,000.

With a $25 copay, you’d pay $25 each visit—no matter how many times you go. That’s predictable, but it doesn’t reduce your overall out-of-pocket spending until you meet your deductible.

Cost Structure

- Deductible: Variable. It depends on your plan and how much healthcare you use.

- Copay: Fixed. You always pay the same amount for the same service.

This means copays are easier to budget for, but they don’t scale with your actual medical expenses. If you have a chronic condition and visit the doctor monthly, copays can add up fast—even if you haven’t met your deductible.

When Each Applies

- Deductible: Applies to most medical services, including hospital stays, surgeries, and diagnostic tests.

- Copay: Typically applies to outpatient services like office visits and prescriptions.

Some services may have both a deductible and a copay. For example, you might pay your full cost until you meet your deductible, then pay a copay for future visits.

How Deductibles and Copays Affect Your Wallet

Understanding how deductibles and copays impact your budget is essential. Let’s look at two common plan types to see how they differ.

High Deductible Health Plan (HDHP) Example

HDHPs are popular for people who want lower monthly premiums and can afford higher out-of-pocket costs. Here’s a sample HDHP:

- Premium: $150/month

- Deductible: $3,000 individual

- Copay: None for most services (after deductible)

- Out-of-Pocket Max: $7,000

You’ll pay $1,800 in premiums over the year. If you have a $2,000 doctor visit, you pay the full amount. After that, your insurance starts covering 80% of costs—but you’re still responsible for 20% until you hit the out-of-pocket maximum.

HDHPs often come with Health Savings Accounts (HSAs), which let you save pre-tax money for medical expenses. That’s a big advantage if you expect high medical costs.

Low Deductible Plan Example

Low deductible plans are ideal for people who want predictable, lower out-of-pocket costs. Here’s a sample:

- Premium: $400/month

- Deductible: $500 individual

- Copay: $20 for primary care, $40 for specialists

- Out-of-Pocket Max: $4,000

Over the year, you’ll pay $4,800 in premiums. But if you visit the doctor six times, you’ll only pay $120 in copays. That’s much more manageable if you have regular healthcare needs.

These plans are less likely to have HSAs, but they offer peace of mind with lower upfront costs.

How to Choose Between High and Low Deductible Plans

Choosing the right plan depends on your health needs and budget. Here’s how to decide.

Ask Yourself These Questions

- Do you have regular medical needs? If you see a doctor often or take daily medications, a low deductible plan may save you money.

- Can you afford to pay more upfront? If you can cover a large bill in a year, an HDHP with an HSA might be better.

- Are you generally healthy? Healthy individuals may prefer HDHPs to save on premiums.

- Do you have a chronic condition? If so, a low deductible plan could reduce long-term costs.

Consider Your Financial Situation

If you’re living paycheck to paycheck, a high deductible plan might be risky. One unexpected surgery could cause financial strain. In that case, a plan with lower out-of-pocket costs—even if the premium is higher—might be wiser.

On the other hand, if you have an emergency fund and want to minimize monthly spending, an HDHP could free up cash flow.

Look at the Total Cost

Don’t just compare premiums. Calculate the total cost: premium + expected deductible + copays. For example:

- HDHP: $1,800 premiums + $3,000 deductible + $500 copays = $5,300 total

- Low Deductible: $4,800 premiums + $500 deductible + $300 copays = $5,600 total

In this case, the HDHP is actually cheaper—even though the monthly premium is lower.

Tips for Managing Deductibles and Copays

Once you understand how deductibles and copays work, you can take steps to manage them better.

Use In-Network Providers

Staying in-network keeps costs down. Out-of-network services often have higher deductibles and no copays. Always check if your doctor is in-network before scheduling.

Track Your Spending

Keep a log of your medical expenses. Use a spreadsheet or app to track how much you’ve paid toward your deductible. This helps you know when coverage kicks in.

Use Preventive Services

Take advantage of free preventive care. Annual checkups, screenings, and vaccines are covered 100% before your deductible—even on high deductible plans.

Consider an FSA or HSA

If you have an HDHP, open an HSA. If you have any plan, consider a Flexible Spending Account (FSA). Both let you save pre-tax money for deductibles, copays, and prescriptions.

Budget for Healthcare

Set aside money each month for medical expenses. Even if you have insurance, unexpected costs can arise. A dedicated healthcare fund helps you avoid debt.

Common Misconceptions About Deductibles and Copays

There are a lot of myths about how deductibles and copays work. Let’s clear them up.

Myth 1: Copays Count Toward Your Deductible

Not always. Some plans do, but many don’t. If your $25 copay doesn’t count toward your $1,000 deductible, you’ll pay it separately. Always check your plan summary.

Myth 2: Once You Meet Your Deductible, Everything Is Free

No. After meeting your deductible, you may still pay coinsurance (a percentage of the cost) until you hit your out-of-pocket maximum.

Myth 3: High Deductible Plans Are Always Bad

Not if you’re healthy and can afford the upfront costs. HDHPs with HSAs offer tax advantages and lower premiums.

Myth 4: Copays Are the Same for All Services

No. Emergency room visits usually have higher copays than primary care visits. Prescriptions vary by drug type and plan.

Conclusion: Make Informed Choices About Your Health Plan

Understanding the difference between medical insurance deductible vs copay is one of the best ways to take control of your healthcare costs. A deductible is your gateway to coverage—the amount you pay before insurance steps in. A copay is a predictable fee for specific services, usually after your deductible is met.

Both are important, but they serve different purposes. Choosing the right plan depends on your health needs, budget, and how you prefer to manage medical expenses. Whether you go for a high deductible plan with an HSA or a low deductible plan with steady copays, the key is to know what you’re signing up for.

Take time to review your plan each year during open enrollment. Ask questions. Compare costs. And don’t hesitate to use tools like cost estimators or speak with a benefits advisor. Your health and wallet will thank you.

Frequently Asked Questions

What is the difference between a deductible and a copay?

A deductible is the amount you pay out of pocket before insurance starts covering most services. A copay is a fixed fee you pay for specific services, like a doctor visit or prescription. Deductibles are cumulative, while copays are per-service.

Do copays count toward your deductible?

It depends on your plan. Some plans allow copays to count toward your deductible, while others don’t. Check your plan summary to be sure.

Can I use my HSA to pay for copays?

Yes, if you have a Health Savings Account (HSA) with a high deductible plan, you can use it to pay for qualified medical expenses, including copays and deductibles.

Are preventive services covered before meeting the deductible?

Yes, most preventive services like annual checkups, vaccines, and screenings are covered 100% before you meet your deductible.

What happens after I meet my deductible?

After meeting your deductible, your insurance usually covers a larger share of your costs—often 80–90%—depending on your plan. You may still pay copays or coinsurance until you reach your out-of-pocket maximum.

How do I know which plan is right for me?

Consider your health needs, budget, and how often you use medical services. If you have regular care needs, a low deductible plan may save money. If you’re healthy and want lower premiums, a high deductible plan with an HSA could be better.