Finding affordable health insurance doesn’t mean sacrificing quality. Best budget friendly medical insurance plans now offer comprehensive coverage with low premiums, high deductibles, and essential benefits—perfect for anyone looking to protect their health without overspending. Whether you’re self-employed, a young professional, or on a tight budget, there are smart, flexible options available today.

Key Takeaways

- Affordable does not mean inadequate. Many low-cost medical insurance plans offer essential benefits, including preventive care, emergency services, and prescription coverage.

- High-deductible plans can be cost-effective. Plans with lower monthly premiums but higher out-of-pocket costs may save money if you rarely use medical services.

- Government programs offer free or low-cost coverage. Medicaid, CHIP, and subsidies through the Health Insurance Marketplace can drastically reduce your insurance costs.

- Short-term plans are an option—but with limits. These plans provide temporary coverage but often exclude pre-existing conditions and essential health benefits.

- Compare plans carefully using official tools. Use the Health Insurance Marketplace (Healthcare.gov) or state-based exchanges to compare plans, costs, and coverage details.

- Consider HSAs for high-deductible plans. Health Savings Accounts let you save tax-free money to pay for qualified medical expenses.

- Shop during open enrollment or special periods. Missing open enrollment? You may qualify for a Special Enrollment Period due to life events like marriage, job loss, or moving.

📑 Table of Contents

- Introduction: Health Insurance on a Budget — It’s Possible

- Understanding What Makes a Plan “Budget Friendly”

- Top Types of Budget-Friendly Medical Insurance Plans

- How to Choose the Right Budget-Friendly Plan for You

- Tips to Maximize Your Savings on Health Insurance

- Common Mistakes to Avoid When Buying Affordable Health Insurance

- Real-Life Examples: How People Saved on Health Insurance

- Final Thoughts: Affordability and Peace of Mind Go Hand in Hand

Introduction: Health Insurance on a Budget — It’s Possible

Let’s face it—medical bills can be terrifying. One unexpected ER visit can cost thousands, and the fear of not being able to afford care often leads people to skip check-ups or avoid treatment altogether. That’s why having health insurance isn’t just a nice-to-have—it’s a necessity. But for many Americans, especially young adults, freelancers, and those working low-wage jobs, the cost of insurance can feel overwhelming.

Here’s the good news: you don’t need to pay top-dollar for quality health coverage. There are plenty of best budget friendly medical insurance plans that balance affordability with meaningful protection. These plans are designed for people who want to stay healthy, avoid financial ruin from medical debt, and still access the care they need—without draining their bank account.

In this guide, we’ll walk you through the different types of affordable health insurance options, how to compare them, and tips to make the most of your coverage. Whether you’re uninsured, underinsured, or just looking to save a few bucks each month, this article will help you find the right plan for your needs and wallet.

Understanding What Makes a Plan “Budget Friendly”

When we talk about “budget-friendly” health insurance, we’re not just talking about low monthly premiums. A truly affordable plan also considers out-of-pocket costs, coverage quality, and how well it fits your lifestyle. Let’s break down what that means.

Visual guide about Best Budget Friendly Medical Insurance Plans

Image source: 184.72.99.137

Low Premiums Are Just the Start

The premium is what you pay every month for your insurance—regardless of whether you use it or not. A low premium sounds great, but if the plan has a high deductible (the amount you pay before insurance kicks in), you could end up spending more out of pocket if you get sick.

For example, a plan might cost $150/month with a $6,000 deductible. That’s only $1,800 per year, but if you need surgery, you could pay up to $6,000 before coverage starts. Compare that to a plan with a $300/month premium and a $1,500 deductible—you pay more monthly, but less when you need care.

So, the best budget friendly medical insurance plans often come from balancing these two costs. For healthy individuals who rarely visit the doctor, a high-deductible plan with low premiums can be a smart choice. For families or people with ongoing health issues, a plan with moderate premiums and lower out-of-pocket costs might be better.

Essential Benefits vs. Extra Perks

Not all insurance plans are created equal. Under the Affordable Care Act (ACA), “qualified health plans” must cover 10 essential health benefits. These include:

- Preventive care (like vaccinations and cancer screenings)

- Emergency services

- Prescription drugs

- Maternity and newborn care

- Mental health and substance use treatment

- Laboratory services

- Pediatric care (including dental and vision for kids)

Some budget plans may cut corners by excluding certain services or limiting provider networks. That’s why it’s important to read the fine print. The best affordable plans still include these core benefits but may charge copays or coinsurance for certain services.

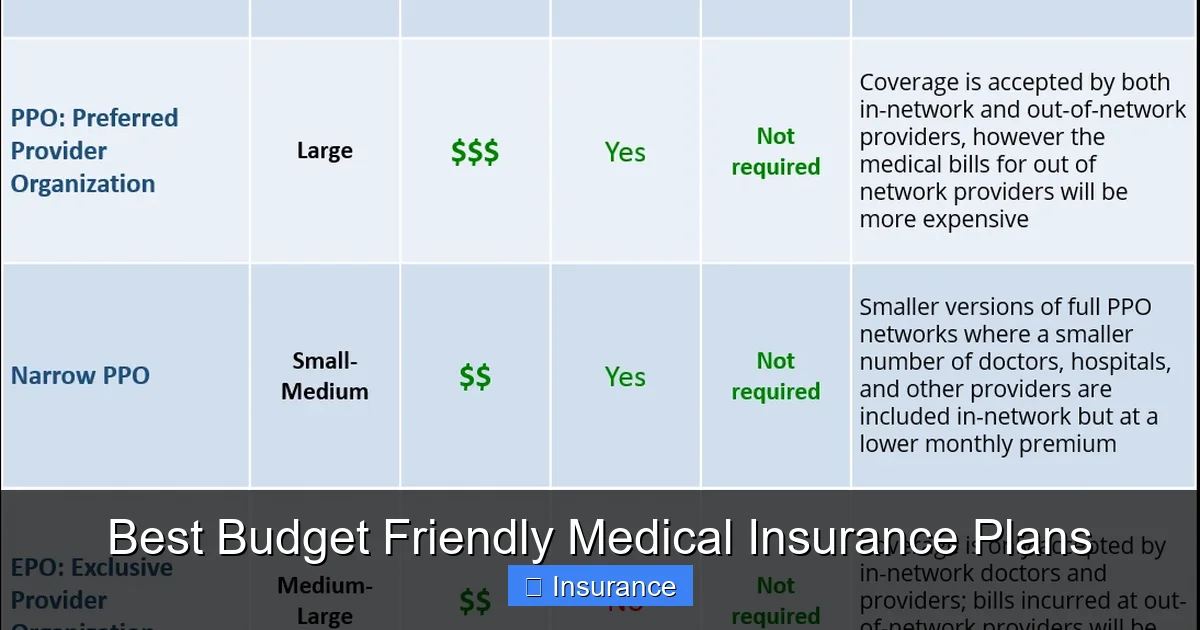

Top Types of Budget-Friendly Medical Insurance Plans

Not all health insurance plans are the same. Depending on your situation, one type might be more affordable than another. Here are the most common options for people on a budget.

Visual guide about Best Budget Friendly Medical Insurance Plans

Image source: mcclaincellars.com

1. Marketplace Plans (ACA-Compliant Plans)

These plans are sold through the Health Insurance Marketplace, either online at Healthcare.gov or through your state’s exchange. All Marketplace plans must follow ACA rules and offer the same 10 essential benefits.

One of the biggest advantages? Subsidies based on income. If you earn less than 400% of the federal poverty level (about $59,000 for a single person or $121,000 for a family of four in 2024), you may qualify for premium tax credits or cost-sharing reductions that lower your monthly payments and out-of-pocket costs.

For example, Maria, a freelance graphic designer making $35,000 a year, used a subsidy to reduce her monthly premium from $420 to $85. She also got a Silver plan with lower copays, making it easier to afford regular doctor visits and prescriptions.

2. High-Deductible Health Plans (HDHPs)

HDHPs have low monthly premiums and high deductibles—often $1,500 to $8,000 or more. But here’s the catch: once you meet the deductible, your insurance covers a large portion of most services.

These plans are ideal if you’re young, healthy, and don’t expect to need frequent medical care. You can pair an HDHP with a Health Savings Account (HSA), which lets you save money tax-free to pay for medical expenses.

Let’s say you choose an HDHP with a $4,000 deductible and $200/month premium. You pay $2,400 per year in premiums. If you never go to the doctor, you save money. But if you have a serious illness, the high deductible could be a burden unless you’ve saved up in your HSA.

3. Short-Term Health Insurance

Short-term plans are designed to last 3–12 months and are often marketed as a “gap” solution for people between jobs or waiting for ACA coverage to start.

They’re usually the cheapest option—premiums can be as low as $50–$100/month. But here’s the downside: they don’t have to cover essential health benefits. They may exclude pre-existing conditions, maternity care, mental health services, and prescription drugs.

Because of these limitations, short-term plans are risky. If you get sick or need ongoing care, you could face huge out-of-pocket costs or be denied coverage altogether.

Still, they can be useful in emergencies. Just don’t rely on them as your main insurance.

4. Catastrophic Plans

Available only to people under 30 or those with a hardship exemption, catastrophic plans have low premiums and very high deductibles (typically over $9,000 for an individual). They’re designed to protect against worst-case scenarios—like a major accident or illness.

These plans cover preventive services (like annual check-ups and vaccines) before you meet the deductible. But for most routine care, you pay full price until you hit the deductible.

Catastrophic plans are rarely the best choice for families or people with chronic conditions. But for young, healthy individuals who want peace of mind against a medical emergency, they can be a surprisingly affordable option.

5. Medicaid and CHIP

Medicaid is a joint federal and state program that provides free or low-cost health coverage to low-income individuals and families. CHIP (Children’s Health Insurance Program) covers kids in families who earn too much for Medicaid but not enough for private insurance.

In 2024, thanks to expanded eligibility under the ACA, many more people qualify. You can apply anytime—there’s no open enrollment period for Medicaid.

To qualify, your income must be below a certain level, which varies by state. For example, in some states, a family of four can earn up to $37,000 a year and still qualify. Coverage includes doctor visits, hospital stays, prescriptions, mental health care, and more—all at little or no cost.

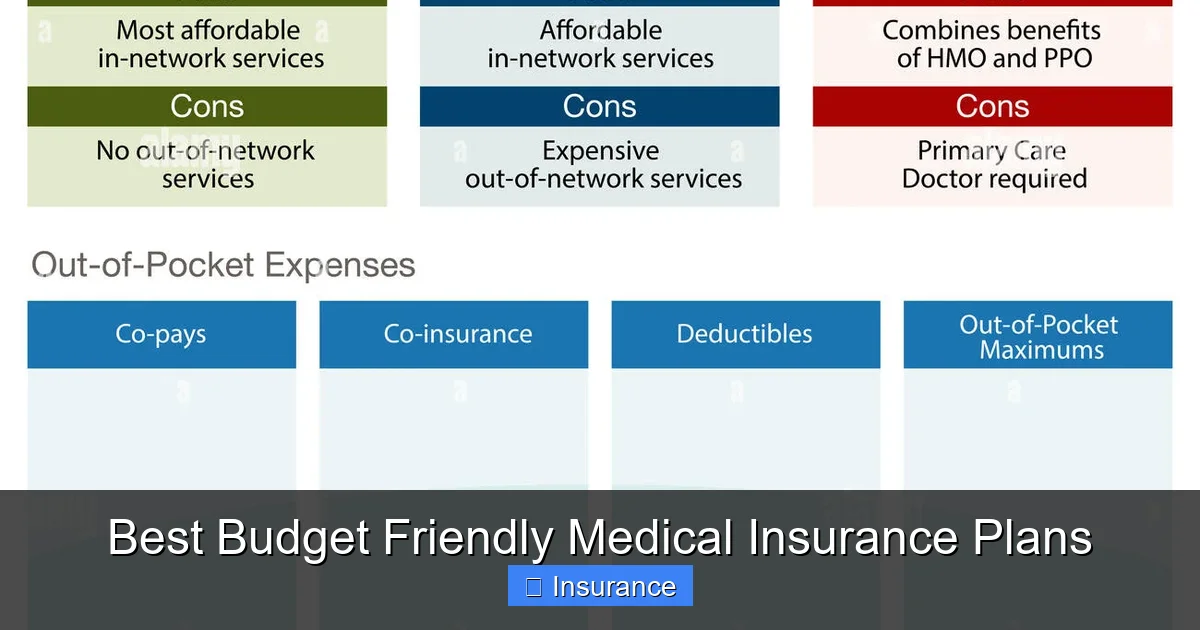

How to Choose the Right Budget-Friendly Plan for You

With so many options, how do you pick the best budget friendly medical insurance plans for your situation? Start by asking yourself a few key questions.

Visual guide about Best Budget Friendly Medical Insurance Plans

Image source: c8.alamy.com

What’s Your Health Status?

If you’re generally healthy and rarely see a doctor, a high-deductible plan or short-term insurance might work. But if you have chronic conditions like diabetes or asthma, or if you’re pregnant, you’ll want a plan with lower out-of-pocket costs and strong coverage for prescriptions and specialist care.

What’s Your Budget?

List your monthly expenses and see how much you can comfortably spend on insurance. Remember, the cheapest plan isn’t always the best if it leaves you with huge medical bills. Aim for a balance between premium and deductible.

Do You Qualify for Subsidies?

Visit Healthcare.gov to estimate your subsidy. Even if you think you make too much, you might qualify—especially if you’re a freelancer with irregular income.

What Doctors and Hospitals Do You Use?

Check if your preferred providers are in the plan’s network. Out-of-network care can cost 2–3 times more, even with insurance. Most budget plans are “narrow network,” meaning they partner with fewer hospitals and clinics—but that can be fine if your local providers are included.

What About Prescriptions and Mental Health?

If you take regular medications or need therapy, make sure the plan covers them. Some low-cost plans have high copays for prescriptions or limit mental health visits. Look for plans with good pharmacy and behavioral health benefits.

Tips to Maximize Your Savings on Health Insurance

Even the best budget friendly medical insurance plans can be optimized to save you even more money. Here are practical tips to stretch your insurance dollar.

Use Preventive Care at No Cost

Under the ACA, all qualified plans must cover preventive services—like annual physicals, flu shots, and cancer screenings—at 100% with no deductible or copay. Take advantage of this. Regular check-ups can catch problems early and save you from expensive treatments later.

Shop Around Every Year

Health insurance changes every year. Premiums, deductibles, and benefits can shift. Use open enrollment (usually November–January) to compare plans and switch if you find a better deal.

Consider a Health Savings Account (HSA)

If you have an HDHP, open an HSA. You can contribute up to $4,150 (2024) for individuals or $8,300 for families. The money grows tax-free and can be used for qualified medical expenses—even after you retire. It’s like a 401(k) for healthcare.

Bargain on Prescriptions

Use pharmacy discount programs, manufacturer coupons, or mail-order services. Generic drugs are often much cheaper than brand-name versions. Some plans also have preferred pharmacy networks that offer lower copays.

Negotiate Medical Bills

If you get a surprise bill, don’t panic. Call the hospital or doctor’s office and ask to speak with a billing representative. Many are willing to reduce charges if you pay in cash or set up a payment plan. You’d be surprised how often they agree.

Use Telehealth Services

Many plans now include telehealth for minor issues like colds, rashes, or anxiety. It’s often cheaper and more convenient than an in-person visit. Check if your plan covers it—and how much you’ll pay.

Common Mistakes to Avoid When Buying Affordable Health Insurance

Even smart shoppers can make costly mistakes when picking insurance. Here’s what to watch out for.

Choosing the Cheapest Plan Without Checking Coverage

Remember: low premium ≠ low cost. A plan that seems cheap might have high copays, limited drug coverage, or no mental health services. Always compare total cost of care, not just the monthly price.

Assuming Short-Term Plans Are Safe

Short-term plans are tempting because they’re cheap—but they’re not designed for long-term protection. If you have a pre-existing condition, you might be denied coverage or charged more. And if you get hospitalized, your plan might not pay.

Missing Open Enrollment or Special Enrollment Periods

If you wait too long, you might miss your chance to enroll. But certain life changes—like getting married, having a baby, losing job-based coverage, or moving—qualify you for a Special Enrollment Period. Don’t miss it.

Not Reviewing Your Plan Annually

Your needs change. You might get married, have a child, or start a new job. Review your coverage every year during open enrollment to make sure it still fits.

Ignoring Provider Networks

Using an out-of-network doctor can cost you hundreds or thousands of dollars. Always check if your providers are in-network before scheduling appointments.

Real-Life Examples: How People Saved on Health Insurance

Let’s look at a few real-world scenarios to see how people found affordable coverage.

Case Study 1: Single Mom on a Budget

Jamila, a 34-year-old teacher in Ohio, made $32,000 a year and had a 5-year-old daughter. She was uninsured because her part-time job didn’t offer benefits. During open enrollment, she visited Healthcare.gov and learned she qualified for a premium tax credit.

She chose a Silver plan with a $250/month premium (down from $520) and a $2,000 deductible. She also got cost-sharing reductions, so her copays were low. Now, her daughter gets dental and vision care at no extra cost, and Jamila can afford her asthma medication. “I finally feel secure,” she says.

Case Study 2: Young Adult Starting a Business

Alex, 26, just launched a freelance design business. With no employer plan, he looked into short-term insurance—but realized it wouldn’t cover his prescription for ADHD medication. He switched to an HDHP with an HSA.

His premium is $180/month, and he contributes $200/month to his HSA. He uses the HSA to pay for prescriptions and doctor visits. “I save money every month, and I know I’m protected if something serious happens,” Alex says.

Case Study 3: Retiree on Fixed Income

Martha, 68, retired and on a fixed income, worried about rising health costs. She applied for Medicaid and was approved. Now, she gets full coverage—including long-term care and home health services—at no cost. “I used to skip pills to save money,” she says. “Now I take them without guilt.”

Final Thoughts: Affordability and Peace of Mind Go Hand in Hand

Finding the best budget friendly medical insurance plans doesn’t mean choosing between your health and your wallet. With the right research, you can protect yourself, your family, and your finances—without overspending.

Whether you go with a subsidized Marketplace plan, a high-deductible HDHP, or Medicaid, the key is to understand your needs and shop smart. Use official resources like Healthcare.gov, compare plans side by side, and don’t be afraid to ask questions.

Remember: health insurance is an investment in your future. A small monthly payment today can prevent a financial crisis tomorrow. And the peace of mind? Priceless.

Frequently Asked Questions

What is the difference between a high-deductible plan and a regular plan?

A high-deductible health plan (HDHP) has lower monthly premiums but a higher deductible—the amount you pay before insurance covers most services. Regular plans usually have higher premiums and lower deductibles, making them better if you expect frequent medical care.

Can I get health insurance if I have a pre-existing condition?

Yes. Under the Affordable Care Act, insurance companies cannot deny coverage or charge more based on pre-existing conditions. This applies to Marketplace plans and most individual plans.

How do I know if I qualify for subsidies?

You can estimate your eligibility on Healthcare.gov using your household size and income. If you earn less than 400% of the federal poverty level, you likely qualify for premium tax credits or cost-sharing reductions.

Are short-term health insurance plans worth it?

Short-term plans are cheap but limited. They often exclude pre-existing conditions, maternity care, and essential health benefits. They’re best used temporarily, not as long-term coverage.

Can I change my health insurance plan anytime?

No. You can only enroll or change plans during Open Enrollment (usually November–January) or if you have a qualifying life event, like marriage, job loss, or moving.

What should I do if I get a surprise medical bill?

Contact the provider’s billing department. Ask about discounts, payment plans, or in-network rates. You can also check if the service was incorrectly coded or if the provider is out-of-network without your knowledge.